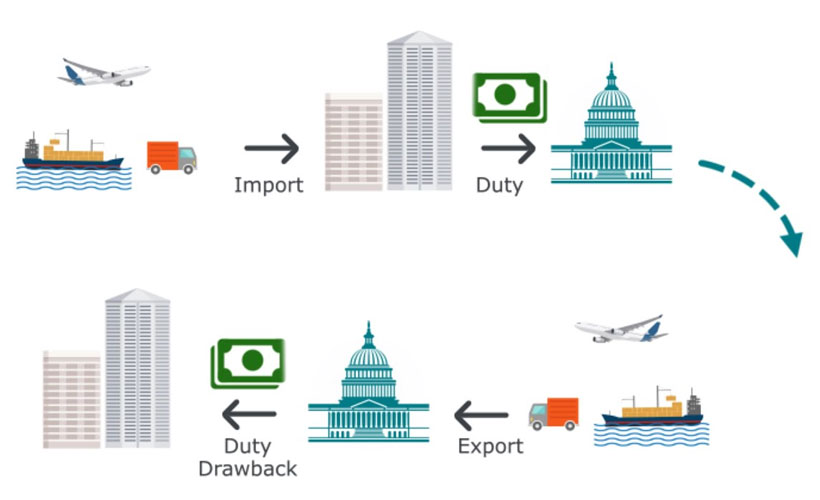

The regulations (found in 19 CFR 190) allow for the transfer of drawback rights when the importer and exporter of record are not the same company. In the industry, this is referred to as Multiple Party or Third-Party Drawback.

For example, Company A imports orange juice from Brazil and pays the duty to Customs before selling the juice domestically with INCO terms Delivered Duty Paid (DDP) to Company B in the United States. Company B then exports the duty paid orange juice from the United States. While either party can submit the claim to Customs, referred to as the drawback claimant, the regulations grant the exporter the first right to submit the to claim drawback.

Specifically, the third-party importer (Company A) can transfer the duty paid imports to the exporter (Company B) with any record that provides the necessary data elements for the exporter to prepare and submit a claim for duty refund. Conversely, if the third-party importer wants to retain the claimant rights, and thus control the preparation and submission of the claim, the importer needs to secure a waiver of drawback rights from the exporter.

Yes I'm Interested